As 2026 began, the direction of global interest rates seemed well-established. Following a series of gradual cuts by both the US Federal Reserve and the Bank of England throughout 2025, economists and analysts widely expected borrowing costs in both countries to fall further over the coming year. The Fed’s December 2025 projections pointed to three additional quarter-point cuts during 2026, which would bring the federal funds rate down to 3%. That outlook was further reinforced by the impending replacement of Fed Chair Jerome Powell in May. His named successor, Kevin Warsh, is widely regarded as more sympathetic to the Trump administration’s repeated calls for lower rates, adding political weight to the case for continued monetary easing.

At the end of last year, the Bank of England was similarly expected to trim its base rate by between 0.25% and 0.75% over the course of the year, offering modest but meaningful relief to UK borrowers. The European Central Bank, having already moved more decisively — cutting its rate to 2% — was forecast to hold steady or announce a single increase this year.

Taken together, the prevailing expectation of falling interest rates was seen as a meaningful tailwind for both global equities and bonds in 2026. With the world economy showing signs of cooling towards the end of 2025, easier monetary policy was expected to provide welcome relief to businesses managing their financing costs and to consumers feeling the pressure of stretched household budgets. That consensus, however, has since been significantly disrupted by events that few anticipated.

The ongoing conflict in Iran has caused modest levels of volatility across global markets. Despite a sharp rise in oil prices and repeated warnings that the Strait of Hormuz — one of the world’s most strategically important shipping lanes, through which a significant share of global oil supply passes — could be closed, markets have remained calmer than they were in the aftermath of Russia’s invasion of Ukraine. That relative stability may partly reflect investor experience with geopolitical shocks, or a belief that the conflict will remain contained. Nevertheless, the situation continues to evolve rapidly, and history shows that geopolitical crises can shift sentiment quickly and without warning.

Since the start of the conflict, bonds have failed to play their traditional role as a safe haven. Rather than rallying as investors sought shelter, bond yields have risen sharply, driven largely by a significant surge in inflation expectations linked directly to the Gulf conflict. The most immediate effect has been visible at petrol stations around the world. At the time of writing, US gasoline prices have climbed more than 26% on average since hostilities began, which feeds into broader cost-of-living pressures. In the UK, the rise in pump prices has been less severe, but heating oil costs have jumped significantly, and if the conflict continues to escalate or simply persists, broader energy price increases look increasingly likely in the weeks ahead.

Higher energy costs, however, are only part of the inflationary picture. Global freight expenses have also climbed considerably as shipping routes are diverted away from the Gulf region, adding substantial delays to supply chains and pushing up both operational costs and insurance premiums for vessels. These pressures were already quietly building before the conflict began. US Producer Price Inflation for February came in at 0.7% month on month, well above market expectations, suggesting that inflationary momentum was gaining traction even before the Gulf crisis fully emerged. The conflict has therefore landed at a particularly sensitive moment for central bank policymakers.

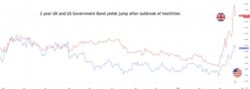

Should oil prices remain elevated for a sustained period, a broader rise in global inflation looks increasingly difficult to avoid, and with it, the next move by the Bank of England and Federal Reserve may be to raise base interest rates. This has already been reflected through higher bond yields, as shown in the graph below, which was produced on 23rd March. The red line is the UK 2-year gilt yield, and the blue line is the US 2-year equivalent.

Source: TradingView March 2026

The critical question for the months ahead is whether these inflationary pressures prove temporary, or whether they begin feeding into wider price increases across the economy, most notably wages. At present, the former still seems the more probable outcome, but a prolonged conflict materially raises the risk of a wage-price spiral not unlike that which took hold in 2022, when central banks were forced into a series of aggressive and economically painful rate hikes.

Rising government borrowing yields are already producing real consequences across the broader economy. Fixed-rate mortgage deals have been withdrawn by lenders since the Iran conflict began, with newly available rates now sitting at their highest level since April 2025. This may place further pressure on the UK housing market.

The strain on public finances is also coming into sharper focus. As existing government gilts mature, the Treasury must refinance at yields that reflect current market conditions. This growing burden raises difficult and politically uncomfortable questions about whether additional tax increases or cuts to public spending may ultimately be required to maintain the confidence of bond markets and preserve the government’s fiscal credibility.

The FAS Investment Committee took the decision last year to continue to focus on bonds with short duration, which was contrary to the stance taken by many analysts who felt it appropriate to take a more neutral position, given the expected path for inflation and interest rates at the time. Given the jump in yields, we are satisfied with our decision, which should help insulate the CDI portfolios from some of the potential downside from higher inflation and potential hikes in base rates. The situation continues to evolve, and naturally, the FAS Investment Committee will continue to monitor economic data and events closely.

If you have concerns about how your portfolio is positioned in these conditions, then speak to one of our independent and experienced advisers.